Considering Financial Accounting

- neyrodriguez0

- Feb 5

- 16 min read

Updated: Mar 30

Accounting is an information and measurement system that identifies, records, and communicates an organization's business activities.

Accounting is called the language of business because it communicates data that helps people make better decisions.

People using accounting are divided into two groups: external user and intenal users

Financial accounting focuses on the external users, and managerial accounting focuses on the internal users.

External users are lenders, investors, nonmanagerial and nonexec employees, labor unions, voters, contributors, suppliers, customers

Internal users are purchasing managers, poduction managers, HR, Service Managers mainly internal management.

Data Analytics and Data Visualization are among the top skills sought by employers which include:

Descriptive - Summarizes and describes events from the past

Diagnostic - Reveals causes of events from the past

Predictive - Preditcs likely events from the future

Prescriptive - Creates action plans to achieve a desire future

A rising type is cognitive analytics which involces AI to analyze and understand data in a way that mimics human cognition.

Remember, for information to be useful, it must be trusted. This demands ethics in accounting.

Ethics are beliefs that separate right from wrong.

Misleading information can lead to a bad decision that can harm workers and or the business.

There is an old saying: GOOD ETHICS IS GOOD BUSINESS.

Fraud Triangle: Ethics under Attach.

The Fraud triangle shows three factors that push a person to commit. fraud.

Opportunity. A person must be able to commit fraud with a low risk of getting caught

Pressure, or incentive. A person must feel pressure or have incentive to commit fraud

Rationalization, or attitude. A person justifies fraud or does not see its criminal nature

THE KEY TO STOPPING FRAUD IS TO FOCUS ON PREVENTION.

It is less expensive and more effective to prevent fraud than it is to detect it. To help prevent, companies set up internal controls.

Financial accounting is governed by concepts and rules known as GAAP or generally accepted accounting principles.

GAAP wants information to have relevance and faithful representation. Relevant affect decisions, faithful means information accurately reflects the business results.

The Financial accounting standards board ( FASB) is given the task of setting GAAP from the SEC or security and exchange commission.

The SEC is a US agency that overseas proper use of GAAP by companies that sell stock and debt to the public.

Our global economy demands comparability in accounting reports. The International Accounting Standards Board ( IASB ) issues International Financial Reporting Standards ( IFRS ) that identify preferred accounting practices.

The FASB and IASB are working to recuce differences between US GAAP and IFRS.

The FASB conceptual framework consist of:

Objectives - To Provide information useful to investors, creditors and others

Qualitative - To require information that has relevance and faithful representation

Elements - To define items in financial statements

Recognition and measurement - To set criteria for an item to be recognized as an element and how to measure it.

There are two types of accounting principles and assumptions. General principles are the

assumptions, concepts, and guidelines for preparing financial statements. Shown in purple and Specific principles are detailed rules used in reporting business transactions and events. Shown in red.

There are four general principles:

Measurement Principle (Cost Principle) Accounting information is based on actual cost. Actual cost is considered objective. This means cash is given for a service, its cost is measured by the cash paid.

Revenue Recognition principle - Revenue is recognized when goods or services are provided to customers and at the amount expected to be received. To recognize means to record it even if the customer promised to pay at a future date called a credit sale.

Expense recognition principle or matching principle. Expense is recognized in the same period as the revenue recognized as a result of that expense. The word incurred is used in accounting to mean that an expense occurred and needs recording.

Full disclosure principle meaning a company reports the details behind financial statements that would impact users decisions. Those disclosures are often in footnotes to the statements.

Accounting Assumptions...

There are 4 accounting assumptions.

Going concern assumption - Accounting information presumes that the business will continue operating instead of being closed or sold out. This means, for example that property is reported at cost and not at liquidating value.

Monetary unit assumption - Transactions and events are expressed in monetary or money units. Monetary units are the US Dollar and not the Mexican Peso

Time period assumption - The life of a company can be divided into time periods such as months and years and useful reports can be prepared for those periods.

Business entity assumption - A business is accounted for separately from other business entities and its owners.

The cost. benefit constraint, or cost constraint says that information disclosed by an entity must have benefits to the user that are greater than the costs of providing it.

Materiality, or the ability of information to influence decisions, is also sometimes mentioned as a constraint.

Some Question and Answer Examples....

Accounting shows two basic aspects of a company: what its owns and what it owes.

Assets are resources a company owns or controls.

The claims on a company's assets - what it owes - are separated into owner (equit) and nonowner (liability) claims.

Together, liabilities and equity are the soure of funds to acquire assets.

Assets are resources a company owns or controls.

The resources are expected to yield future benefits.

Examples are a web server for an online service company, or land for a vegetable grower.

Assets include, cash, supplies, equipment, land and accounts receivable.

Receivables are assets that promise a future inflow of resources.

Liabilities are creditors claims on assets.

These claims are obligations to provide assets, products or services to others.

A payable is a liability that promises a future outflow of resources. Examples are wages payable to workers, accounts payable to suppliers, notes or loans payable to banks and taxes.

Equity is the owners claim on assets and is equal to assets minus liabilities.

Equity is also called net assets or residual equity.

The relation of assets, liabilities and equity is shown in the accounting equation.

We can separate equity into four parts to get the EXPANDED ACCOUNTING EQUATION.

For a noncorporation: Equity = Owners Capital - Owners Withdrawals + Revenues - Expenses

For a Corporation: Equity = Contributed Capital + Retained Earnings + Revenues - Expenses - Dividends

Investment of $30k cash in a new company in exchange for its common stock. Notice, cash and equity each equals to each other $30k.

Then we purchase supplies for $2,500.

This transaction is an exchange of cash, an asset, for another kind of asset, supplies.

Let's spend $26,000 to acquire equipment for testing in the factory. This is exchange of one asset, cash, for another asset, equipment. The purchase changes the makeup of assets but does not change the asset total. The account equation remains in balance.

The company decides to purchase more supplies for the cost of $7,500. But notice we only have $1,500 in cash. We arrange to purchase the supplies on credit. Thus we are agreeing to purchase the supplies in exchange for a promise to pay for them later. This purchase increases assets by $7,100 in supplies and liabilities called accounts payable increase for the same amount.

We are planning to earn revenue for consulting services of $4,200 cash.

The accounting equation reflects this increase in cash of $4,200 and in equity of $4,200. This increase in equity is shown in the far right column under Revenue because the cash received is earned by providing consulting services.

Next we pay $1,000 to rent a facility for the month of December. We also pay biweekly salary to our only employee for $700. The costs of both rent and salary are expenses, not assets.

The accounting equation shows that both transactions reduce cash and equity. The far right column shows these decreases as expenses.

The company provides consulting services of $1,600 and rents its test facilities for an additional $300. This transaction creates a new asset called accounts receivalbe which is increased instead of cash because the payment has not yet been received.

Equity is increased from the two revenue components.

Remember, we record the revenue when the work is performed, not necessarily when cash is received.

When we receive the cash a few weeks later, it does not change the total amount of assets and does not affect liabilities or equity.

It converts the receivable ( an asset ) to cash ( another asset ).

It does not create new revenue. Revenue was recoginized when the service was performed.

Point: Receipt of cash is not always a revenue.

We pay $900 cash as partial payment for earlier $7,100 purchase of supplies.

This transaction decreases my cash and my liability. Equity does not change.

This event does not create an expense even though cash flows out.

Instead the expense is recorded when FastForward uses these supplies?

Next we declare and pay out $200 cash dividend to owners.

Dividends decreases equity aren not reported as expenses because they do not help earn revenue. Because dividends are not expenses, they are not used in computing net income.

CHAPTER 2

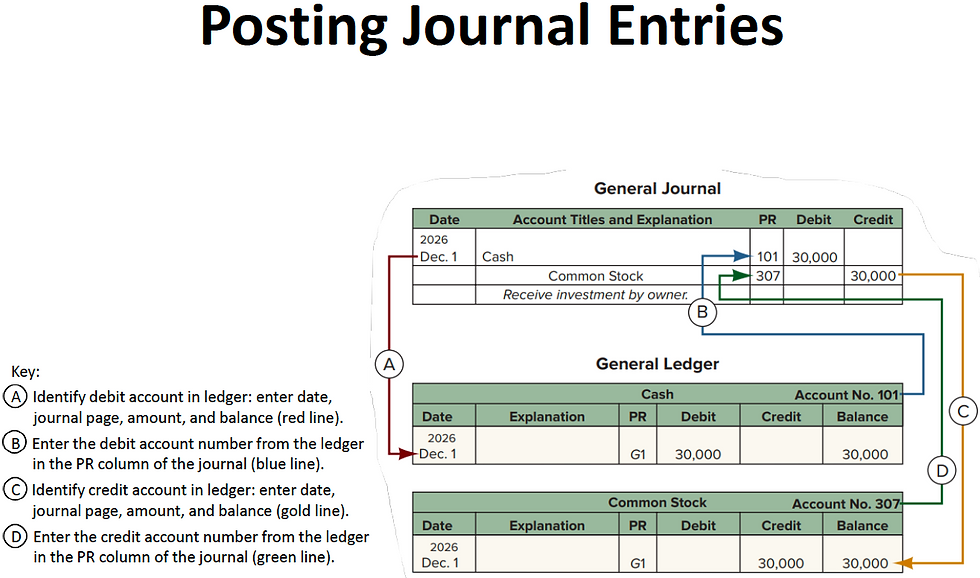

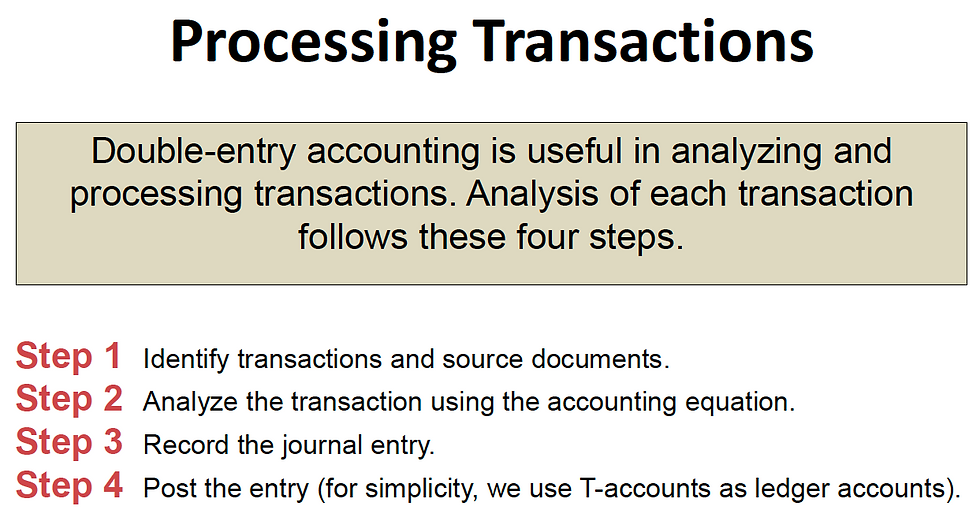

Business transactions and events are the starting points of financial statements. The process to go from transactions and events to financial statements includes:

Source documents identify and describe transactions and events entering the accounting system.

The can be in the form of sales receipts, checks, purchase orders, bills from suppliers, payroll records and bank statements.

An account is a record of increases and decreases in a specific asset, liability, equity, revenue or expense.

The general ledger or simply ledger is a record of all accounts and their balances.

Remember, Dividends and Expenses reduce your equity.

Unearned revenue is a liability that is recorded when customers pay in advance for products or services.

For example a deposit or retainers. Other examples are magazine subscriptions collected in advanced by a publisher, rent collected in advance by a landlord, and season ticket sales by sports teams.

The seller would record these in liability accounts such as Unearned subscriptions and Unearned Rent. When products and services are later delivered, unearned revenue is transferred to revenue.

Remember, the owners claim on a company's assets is called equity, stockholder's equity or shareholders equity.

Equity is the owners residual interest in the assets of a business after subtracting liabilities.

Equity is impacted by 4 types of accounts:

When an owner invests in a company, it increases both assets and equity. The increase to equity is recorded in the account titled common stock. Owners investments are not revenues of the business.

When a corporation distributes assets to its owners, it decreases both company assets and total equity.

The decrease to equity is recorded in an account titled DIVIDENDS.

Dividends are not expenses of the business; they are simply the opposite of owners investments.

The collection of all accounts and their balances is called a ledger or general ledger. A company's size and diversity of operations affect the number of accounts needed.

A small company can have 20; a large cone a 1000.

The chart of accounts is a list of all ledger accounts with an identification number assigned to each account.

Common number system for the chart of accounts.

Assets (10000 series)

10100 – Cash

10200 – Accounts Receivable

12000 – Inventory

15000 – Equipment

16000 – Accumulated Depreciation

Liabilities (20000 series)

20100 – Accounts Payable

22000 – Credit Card Payable

23000 – Payroll Liabilities

25000 – Loans Payable

Equity (30000 series)

30100 – Owner’s Capital

30200 – Retained Earnings

Revenue (40000 series)

40100 – Product Sales

40200 – Service Revenue

Cost of Goods Sold (50000 series)

50100 – Materials

50200 – Direct Labor

Operating Expenses (60000 series)

60100 – Salaries

61000 – Rent

62000 – Utilities

63000 – Marketing

65000 – Insurance

DEFINING DEBITS AND CREDITS AND EXPLAINING DOUBLE ENTRY ACCOUNTING

Remember, only Assets, Expenses and Dividends go up or increase with Debit

Remember, you record your transactions or Journalize them by inserting them in the General Journal, then these go into the General Ledger, then into your Subsidiary Ledger if you are keeping them etc.

CHAPTER 3

The value of information is linked to its timeliness. The time period assumption presumes that an organization's activities can be divided into specific time periods such as a month, a three month quarter, six month or a year. Most organizations use a year as their primary accounting period.

The annual reporting period is not always a calendar year ending on Dec 31. An organization can use a fiscal year consisting of any 12 consecutive months or 52 weeks.

Companies with little seasonal variation in sales often use the calendar year as their fiscal year.

Companies that have seasonal variations in sales often use a natural business year end, which is when sales are at their lowest level for the year.

For example the natural year for retailers such as target or nordstrom ends around Jan 31 after the holidays.

Accrual basis accounting records revenues when cash is received and records expenses when cash is paid. Cash basis income is cash receipts minus cash payments.

Cash basis accounting records revenues when cash is received and records expenses when cash is paid.

Most agree that accrual accounting better reflects business performance than cash basis accounting. Accrual accounting also increases the comparability of financial statements from period to period.

A cash basis income statement for Dec 2026 reports insurance expense of $2400. The cash basis income statements for 2027 and 2028 report no insurance expense. The cash basis balance sheet never report a prepaid insurance asset because it is immediately expensed.

Also cash basis income for 2026-2028 does not match the cost of insurance with the insurance benefits received for those years.

Recognizing Revenues and Expenses

We divide a company's activities into time periods, but not all activities are complete when financial statements are prepared.

Thus adjustments are required to get proper account balances.

We use two principles in the adjusting process: Revenue recognition and expense recognition.

The revenue recognition principle requires that revenue be recorded when the goods or services are provided to customers and at an amount expected to be received from customers.

The expense recognition (or matching) principle requires that expenses be recorded in the same accounting period as the revenues that are recognized as a result of those expenses. This matching of expenses with the revenue benefits is a major part of the adjusting process.

Framework for Adjustments

There are four types of adjustments for transactions that extend over more than one period.

Adjustments are made using a 3-step process:

Step 1: Determine what the current account balance equals.

Step 2: Determine what the current account balance should equal.

Step 3: Record an adjusting entry to get from step 1 to step 2.

DEFERRAL OF EXPENSES ALSO CALLED PREPAID ASSETS NOT A LIABILITY

Other prepaid expenses such as prepaid rent and prepaid advertising, are accounted for exactly as insurance and supplies are.

Some prepaid expenses are both paid for and fully used up within a single period.

One example is when a company pays monthly rent on the first day of each month. In this case, we record the cash paid with a debit to rent expense instead of an asset account.

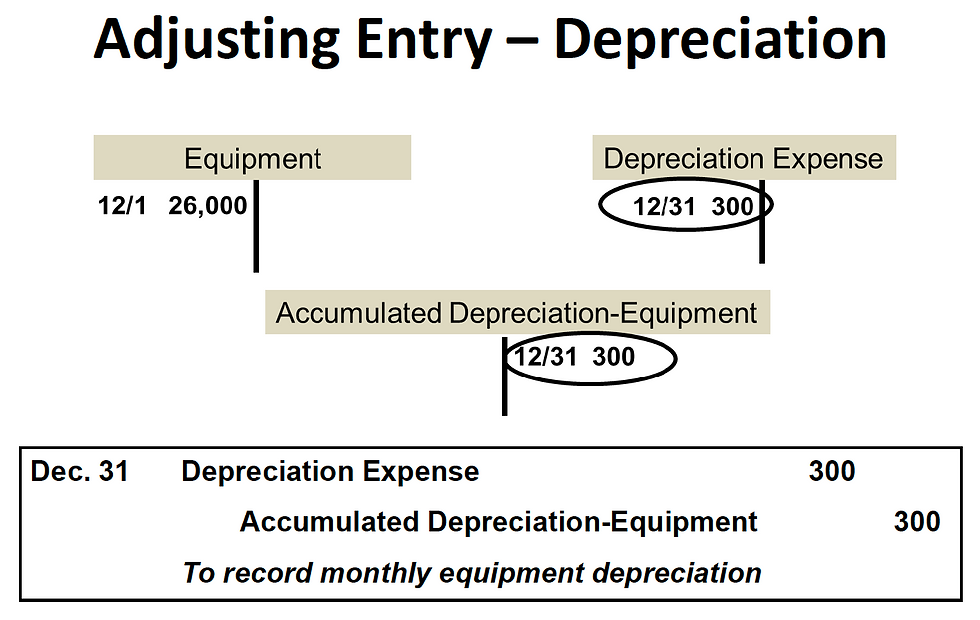

DEPRECIATION

A special category of prepaid expenses is plant assets, also called Property, Plant & Equipment ( PP&E ). Plant assets are long term tangible assets used to produce and sell products and services.

Examples include buildings, machines, vehicles and equipment.

Plant assets provide benefits for more than one period.

All plant assets ( excluding land ) eventually wear out or become less useful.

The costs of plant assets are gradually reported as expenses in the income statement over the assets useful lives ( benefit periods ).

Depreciation is the allocation of the costs of these assets over their expected useful lives, but it does not necessarily measure decline in market value.

Depreciation expense is recorded with an adjusting entry similar to that for other prepaid expenses.

EXAMPLES:

DEFERRAL OF REVENUES ALSO REFERED TO AS A LIABILITY NOT AN ASSET

Unearned revenue is cash received in advance of providing products and services. Unearned revenues, or deferred revenues are liabilities.

When cash is accepted, an obligation to provide products or services is accepted.

We defer or postpone, reporting amounts received as revenues until the product or service is provided.

As products or services are provided, the liability decreases and the unearned revenues become revenues.

Adjusting entries for unearned revenue decrease the unearned revenue (balance sheet) account and increase the revenue ( income statement ) account.

Unearned revenues are common in sporting and concert events.

For example, when the Boston Celtics receive cash from advance ticket sales, they record it in an unearned revenue account called Deferred Game Revenues.

The Celtics record revenue as games are played.

ASSETS (+ $3000 ) = LIABILITIES (+ $3000 ) + EQUITY

ACCRUED EXPENSES. THIS IS A LIABILITY

Accrued expenses, or accrued liabilities are costs that are incurred in a period that are both unpaid and unrecorded.

Accrued expenses are reported on the income statement for the period when incurred.

Adjusting entries for recording accrued expenses increase the expense (income statement) account and increase a liability (balance sheet) account.

This adjustment recognizes expenses incurred in a period but not yet paid.

Common examples of accrued expenses are:

Salaries, interest, rent, and taxes.

For example: Property Taxes

You debit Property Taxes ( the expense ) and you credit the Accrued Property Taxes.

Salaries expense of $1610 is reported on the December income statement, and $210 of salaries payable (liability) is reported in the balance sheet.

Salaries expense of $1610 is reported on the December income statement, and $210 of salaries payable (liability) is reported in the balance sheet.

Remember accrued expenses at the end of one accounting period result in cash payment in a future period. Notice above that on Jan 9th, the first payday of the next period, the above entry settles the accrued liability salaries payable and records salaries expense for seven days of work in January.

ACCRUED Interest Expense

Companies accrue interest expense on notes payable (loans) and other long-term liabilities at the end of a period.

Interest expense is incurred as time passes.

Unless interest is paid on the last day of an accounting period, we need to adjust for interest expense incurred but not yet paid.

This means we must accrue interest cost from the most recent payment date up to the end of the period.

The formula for computing accrued interest is:

Principal amount owed x Annual Interest Rate x Fraction of year since last payment

If a company has $6000 loan from a bank at 5% annual interest, then 30 days accrued interest expense is $25 - computed as:

$6000 x 0.05 x 30 / 360

The adjusting entry debits interest expense for $25 and credits interest payable for $25.

Interest computations use a 360 day year, called the bankers rule.

ACCRUED REVENUES. This one is an ASSET not a LIABILITY

DEFFERED EXPENSES OR PREPAID ASETS AND ACCRUED REVENUES ARE THE ONLY ASSETS ON THIS CATEGORY.

Accrued revenues are revenues earned in a period that are both unrecorded and not yet received in cash or other assets.

An example is a technician who bills customers after the job is done.

If one third of a job is complete by the end of a period, then the technician must record one third of the expected billing as revenue in that period even though there is no billing or collection.

Accrued revenues are also called accrued assets.

An unadjusted trial balance is a list of accounts and balances before adjustments are recorded.

An adjusted trial balance is a list of accounts and balances after adjusting entries have been recorded and posted to the ledger.

Notice that an account can have more than one adjustment, such as for consulting revenue. Some accounts might not require adjustment for this period for example accounts payable. Notice that consulting has more than one adjustment.

We can prepare financial statements directly from information in the adjusted trial balance.

See below how for example revenue and expense balances are transferred from the adjusted trial balance to the income statement ( red ).

Use the following adjusted trial balance of Magic Company to prepare its December 31 year end:

1 - Income Statement

2 - Statement of Retained Earnings

3 - Balance Sheet ( unclassified )

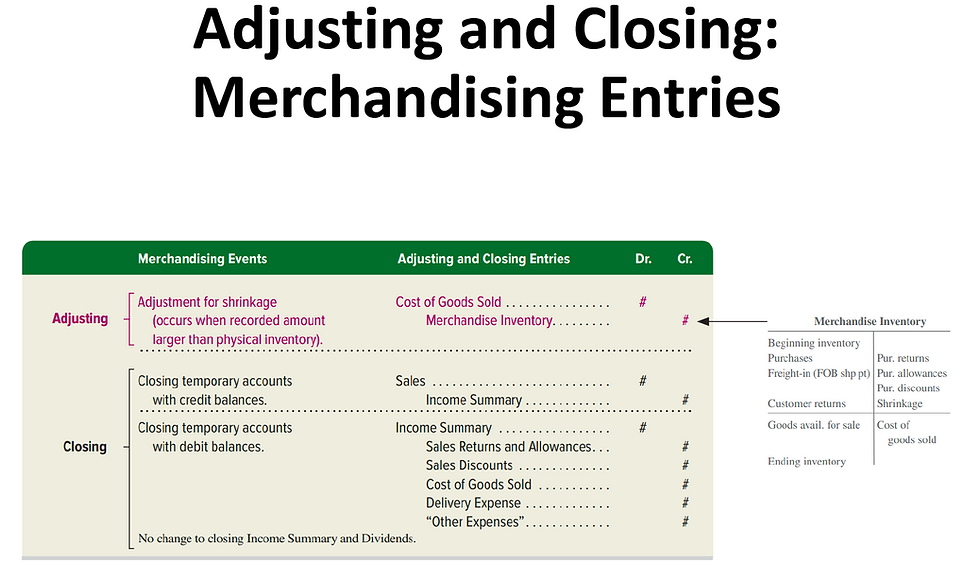

PREPARE CLOSING ENTRIES AND A POST - CLOSING TRIAL BALANCE

The closing process occurs at the end of an accounting period after financial statements are completed.

In the closing process we 1) identify accounts for closing, 2) record and post the closing entries, and 3) prepare a post closing trial balance.

The closing process has two purposes.

First, it resets revenue, expense, and dividends account balances to zero at the end of each period. This is done so that these accounts can properly measure income and dividends for the next period.

Second, it update the balance of the retained earnings account, which matches that reported in the balance sheet and the statement of retained earnings.

Temporary accounts relate to one accounting period. They include all income statement accounts, the dividends account, and the income summary account.

They are temporary because such accounts are used for a period and then closed at period end. The closing process applies only to temporary accounts.

Permanet accounts report on activities related to one or more future accounting periods. They include asset, liability, and equity accounts ( all balance sheet accounts ).

Permanent accounts are not closed each period and carry their ending balance into future periods.

RECORDING CLOSING ENTRIES

Closing entries transfer the end of period balances in revenue, expense, and dividends accounts to the permanent retained earnings account.

Closing entries are necessary at the end of each period after financial statements are prepared because:

- Revenue, expense, and dividends accounts must begin each period with zero balances.

- Retained earnings must reflect prior periods revenues, expenses, and dividends.

For example, if apple did not make closing entries, prior year revenue from iphone sales would be included with current year revenue.

An income statement reports revenues and expenses for an accounting period.

Dividends are also reported for an accounting period.

Because revenue, expense, and dividends accounts record information separately for each period, they must start each period with zero balances.

Retained earnings is the only permanent account - meaning it is not closed, but it does have income summary closed to it.

1 and 2 - To close revenue and expense accounts, we transfer their balances to income summary. Income summary is a temporary account only used for the closing process that contains a credit for total revenues and gains and a debit for total expenses and losses.

3 - The income summary balance, which equals net income or net loss, is transferred to the retained earnings account.

4 - The dividends account balance is transferred to the retained earnings account. After closing entries are posted, the revenue, expense, dividends, and income summary accounts have zero balances and are said to be closed or cleared.

POST CLOSING TRAIL BALANCE

A post-closing trial balance is a list of permanent accounts and their balances after all closing entries.

Only balance sheet ( permanent ) accounts are on a post-closing trial balance.

A post-closing trial balance verifies that:

1 - total debits equal total credits for permanent accounts

2 - all temporary accounts have zero balances

CLASSIFIED BALANCE SHEET.

Remember, a classified balance sheet breaks assets and liabilities into categories, usually based on time ( within 1 year vs. more than 1 year ).

An unclassified balance sheet broadly groups accounts into assets, liabilities, and equity.

An important classification is the separation between current ( short term ) and noncurrent ( long term ) for both assets and liabilities.

PROFIT MARGIN

A useful measure of a company's operating results is the ratio of its net income to net sales. This ratio is called profit margin, or return on sales, and is computed:

The profit margin ratio tells you how much profit a company keeps from each dollar of revenue.

In Simple terms: It shows how efficiently a company turns sales into profit.

The profit margin ratio tells you:

“Out of every dollar of sales, how much does the company actually keep?”

The current ratio tells you whether a company can pay its short-term bills with its short-term assets.

In simple terms:

It measures a company’s short-term financial health (liquidity).

✅ Above 1.0

The company can cover its short-term obligations.

⚠️ Below 1.0

The company may struggle to pay short-term bills.

🤔 Too High?

A very high ratio (like 4 or 5) could mean:

Too much idle cash

Poor use of assets

CHAPTER 4

Think of PERIODIC as of the end of the Period.

Lets analyze and record transactions for merchandise sales using a perpetual system

DEALING WITH CASH EXCESS ON REGISTER AND PETTY CASH

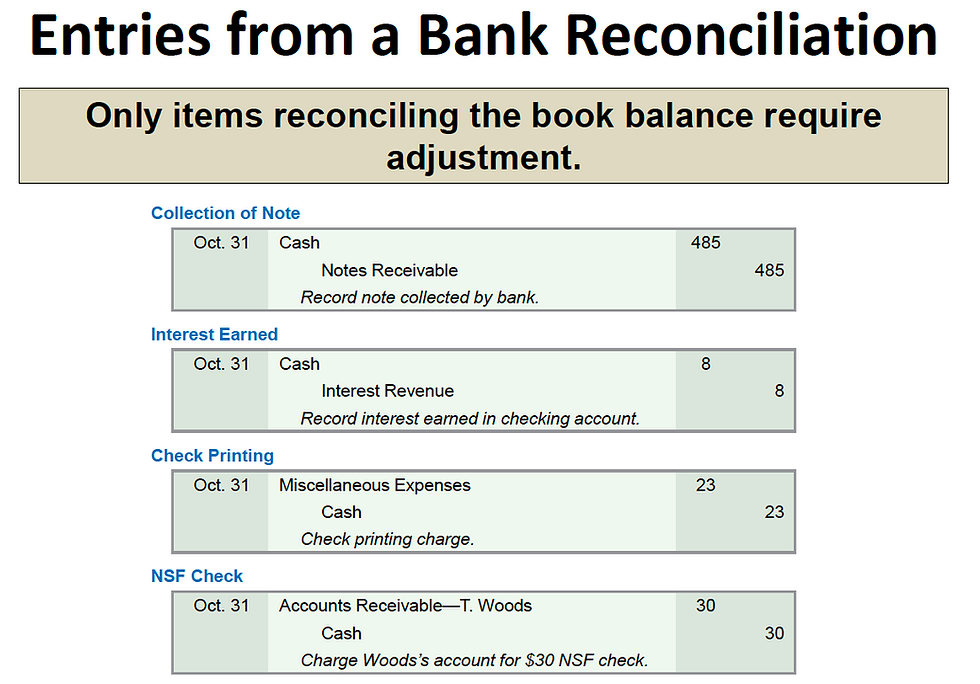

BANK RECONCILIATIONS

The Days’ Sales Uncollected Ratio (also called Days Sales Outstanding – DSO) measures how many days, on average, a company takes to collect cash from its credit sales.

Formula

Days’ Sales Uncollected=Accounts ReceivableNet Credit Sales×365Days’ Sales Uncollected=Net Credit SalesAccounts Receivable×365

🧠 What it means (simple idea)

It tells you how long customers take to pay

Think of it as:

“On average, how many days does it take me to get paid after I make a sale?”

📊 Example

Accounts Receivable = $50,000

Net Credit Sales = $200,000

=50,000/200,000×365=91.25 days

👉 This means it takes about 91 days to collect cash.

👍 How to interpret it

Lower number = GOOD

Faster collections

Better cash flow

Higher number = BAD (usually)

Customers are slow to pay

Possible collection problems

⚠️ Important notes

Compare it with:

Previous years (trend)

Industry average

A high number isn’t always bad if the company intentionally offers long credit terms

💡 Quick intuition

If DSO = 30 days → customers pay quickly

If DSO = 90+ days → cash is tied up, potential risk

Comments